phonepe gold sip pt 1&2

Personalised onboarding for the Gold SIP feature on one of India's largest payment platforms.

00

problem

PhonePe has a Gold SIP feature. People land on it. Then they leave without starting. That's not an awareness problem. It's trust. Digital gold is invisible. You can't hold it, see it, or feel it. And in a country where gold means security, tradition, and wealth passed down a family line, invisible just isn't good enough.

solution

Personalised onboarding, built around what the research actually said about each audience, not just what the product offers.

One naming note. PhonePe calls this Gold Savings, and the monthly version Monthly Gold Savings. That's a mouthful to repeat, so throughout this case study I'll call it Gold SIP. Since "SIP" is genuinely the common term for a monthly savings plan in India, so no one reading it will be confused.

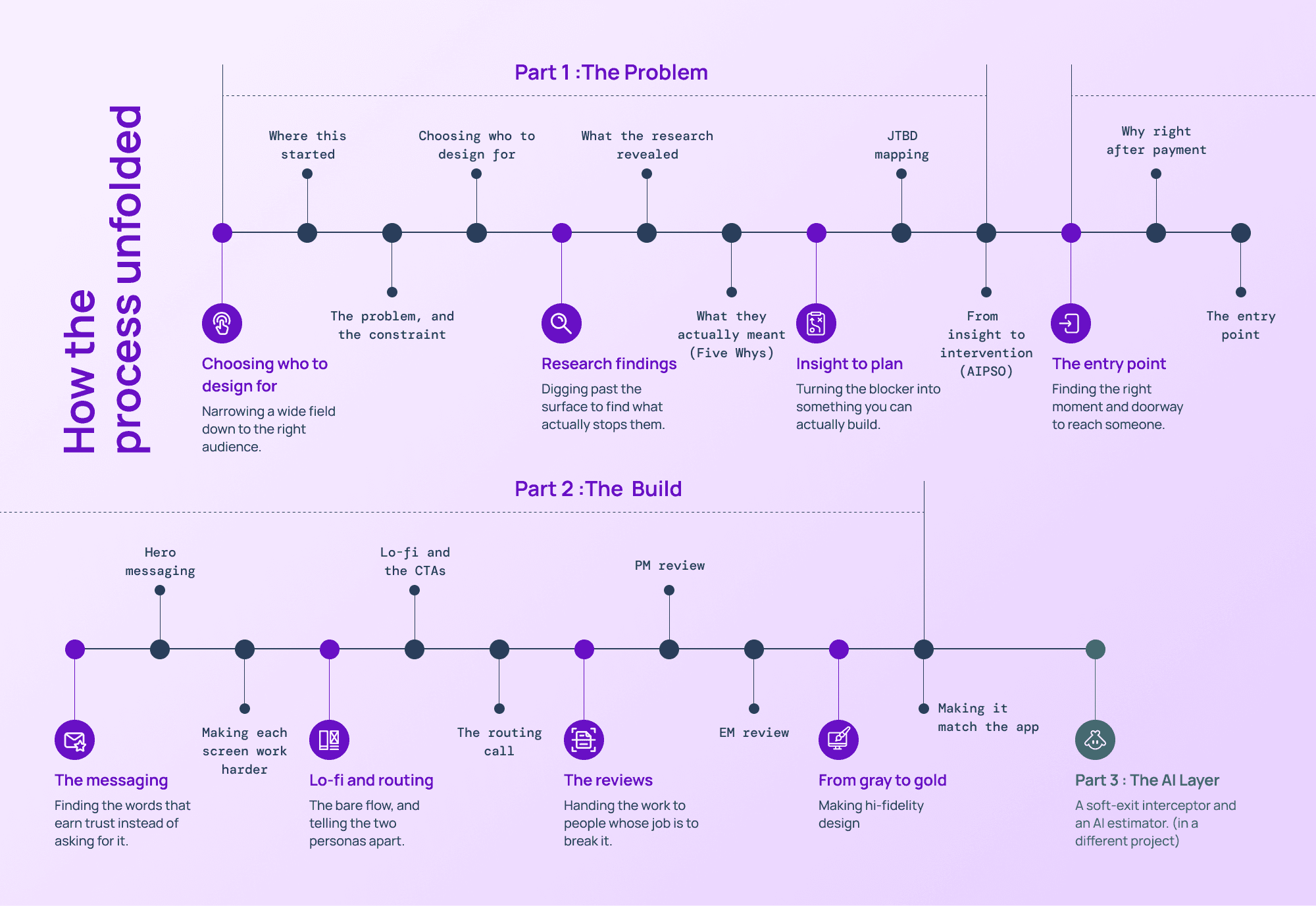

Choosing who to design for

Where this started

This project follows the process Rajat Patel taught across two sessions of his Product Thinking Workshop. He used to work at PhonePe. Session one gave me the problem statement and the JTBD and AIPSO frameworks. Session two was a live demo built with Claude: five personas, a question-prompt-output-review workflow, a simulated PM review, a simulated engineering review.

One line of his stuck with me, word for word:

"Generic onboarding optimizes for completion. Great onboarding optimizes for conviction."

The five personas and his JTBD came from that workshop. Rather than take his findings as given, I ran my own interviews and worked the analysis myself, to see where I'd land independently. I came out close to him, which was a good sign I was reading the users right, but the findings here are mine. From there it's all my own work: I cut the five personas to two, made the design calls, and ran the PM and EM reviews.

To accommodate the FigJam assets here, boards have been redesigned and refined. You can view the full FigJam file by [clicking this link].

The problem, and the constraint

People land on Gold SIP and leave without starting.

The thing shaping the whole project was Diwali. It's the one time of year Indians are most primed to buy gold, culturally and emotionally. But that pull only works on someone who already owns the ritual. The Festive Buyer does. They've been buying gold every year for as long as they can remember. The First Time Buyer hasn't.

And here's the part that's easy to miss. Gold itself isn't foreign to the First Time Buyer. Most of them grew up watching a parent buy it, so the metal carries no mystery. What's unfamiliar is investing. They just haven't made that first move yet, in any form. Gold happens to be the least scary door into something bigger they've never started.

So forcing a Diwali angle onto them would mean handing them a milestone they haven't earned. I kept it out of that flow completely.

I also kept the scope narrow on purpose. Not discovery. Not the payment flow. Just onboarding, starting the second a user lands on Gold SIP.

Choosing who to design for

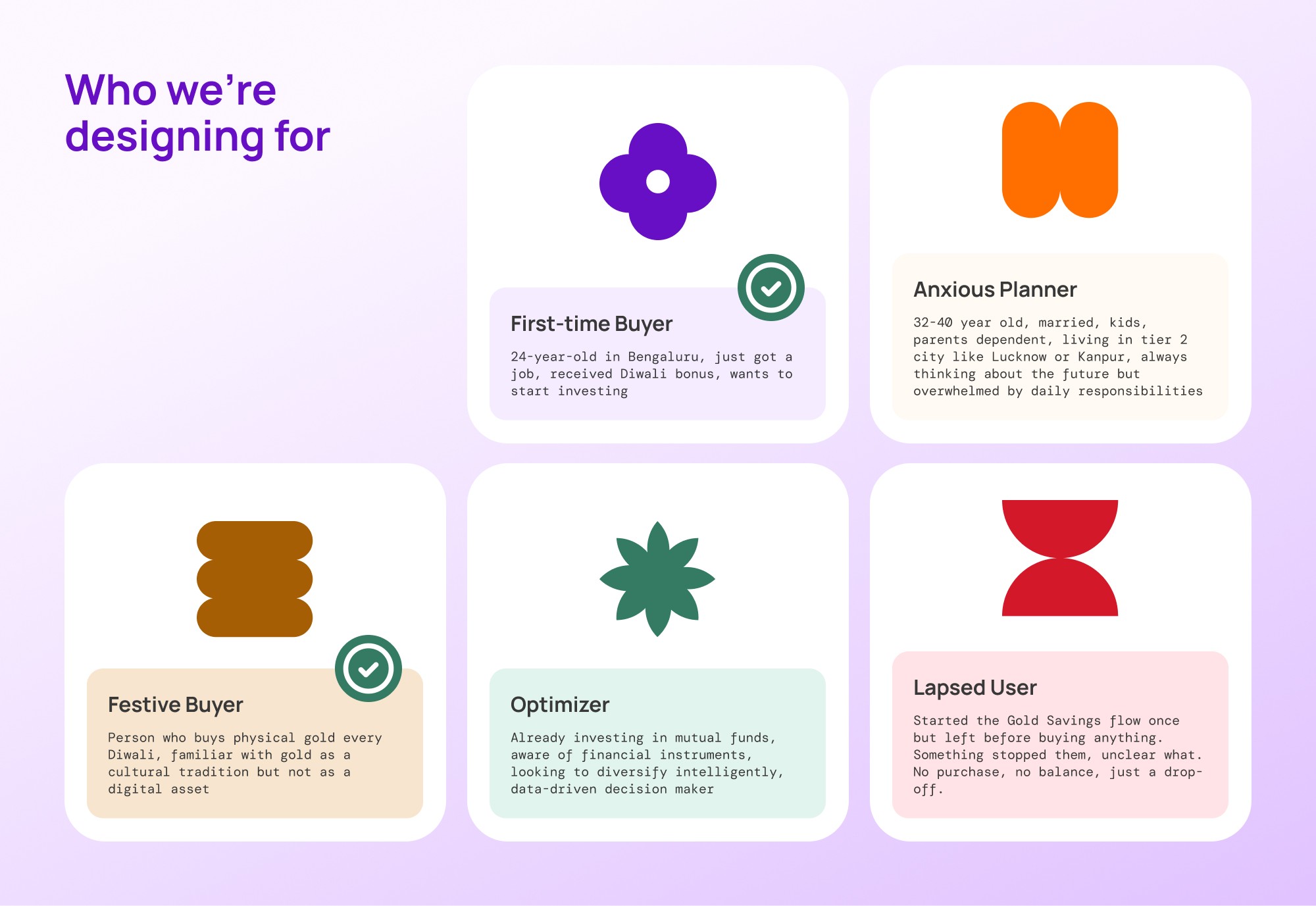

Five personas came out of a structured exercise. Rajat fed PhonePe's context and existing user data categories into Claude, then reviewed and refined what came back instead of taking it at face value.

First Time Buyer

Festive Buyer

Anxious Planner

Optimizer

Lapsed User

Designing well for all five would've meant designing well for none. So I picked the two that sit at opposite ends of the same problem: First Time Buyer and Festive Buyer.

The split isn't just emotional, it's demographic. First Time Buyer skews tier 1, early career, someone in their first job who's never invested in anything. Festive Buyer skews tier 2, older, settled, already spending real money on physical gold every year without fail. Neither has ever bought digital gold, but for opposite reasons. One hasn't invested in anything at all. The other has bought physical gold for years and sees no reason to trust a version they can't hold.

I didn't drop the other three to make life easier. The Optimizer turned out to have a data problem, not a trust problem. They want numbers and projections before any emotional pitch lands, which is exactly what the AI layer solves later, not onboarding. The Anxious Planner's blocker was decision fatigue, a different problem entirely. Keeping either one would've blurred the contrast the whole project leans on.

Research findings

What the research revealed

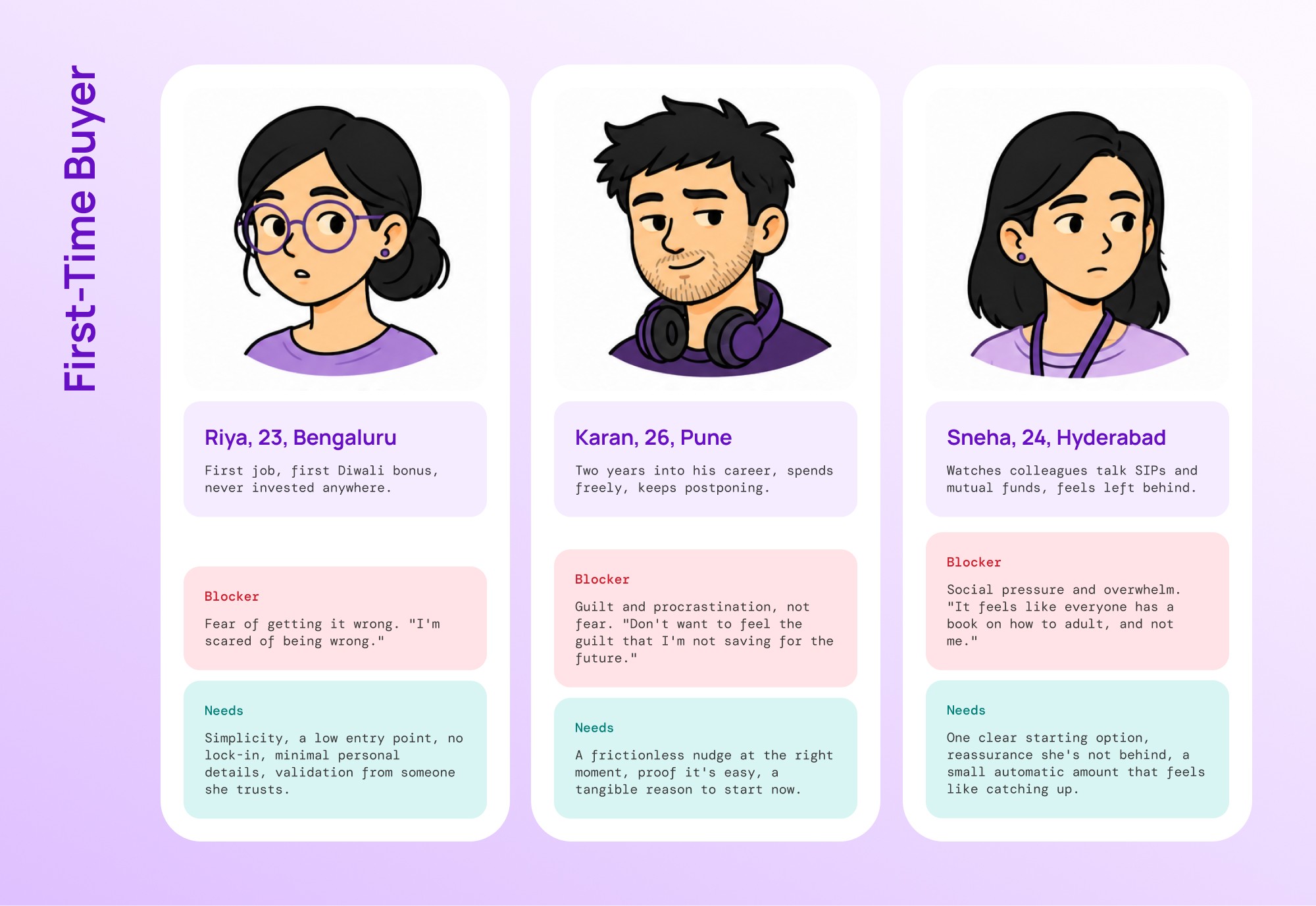

Real interviews weren't possible on the timeline, so I built six structured sub personas instead, using Gemini to generate and pressure-test them. Riya, Karan, and Sneha under First Time Buyer. Ramesh, Sunita, and Vikram under Festive Buyer. I interviewed them like real people: ten core questions on gold, trust, and money, plus four more for the Festive group on what physical gold means to them.

The full interview set is here.

Two things came out. An emotional blocker, different for almost everyone. And a set of practical needs, consistent inside each persona.

The First Time Buyer's label hides a lot. Riya froze on fear, investing still felt like gambling. Karan froze on guilt, he'd put off saving for years. Sneha froze on social pressure, watching peers talk SIPs and feeling behind. Three different reasons to freeze, one bucket.

But underneath, they wanted the same things. Make it easy to start. Let them begin small. Keep the information clear. Go easy on the personal data. And let them pull their money back out without a fight.

The Festive Buyer had range too, but not a full split. Ramesh and Sunita both needed proof that digital gold could still carry a duty owed to family. Vikram sat apart, wanting government backing before anything else, which is part of why I left the Optimizer out as a separate persona. That instinct already lived inside Festive Buyer's research.

Their practical needs were sharper. Does it convert back to real money or gold, easily? Is it government backed? Where's it stored? Is it pure, and who certifies that? If something goes wrong, who's responsible? They've trusted physical gold their whole lives because it answers all of that on its own. Digital gold has to answer it out loud.

The emotional blocker told me what to say. The practical needs told me what to prove.

What they actually meant

The interviews gave me friction points. Five Whys got me underneath them.

The method is simple. You take a complaint and ask why. Then you ask why again about the answer. You keep going until you hit something the user can't explain away, the actual belief driving everything above it. I ran it on each persona separately, comparing the three interviews inside each group so I was chasing patterns, not one person's opinion.

For the First Time Buyer, the surface frictions were the practical ones. It needs knowledge to start. Traditional gold takes a big sum. Don't want to risk money on something unfamiliar. Don't want to hand over PAN and salary details.

Every chain bottomed out in the same place. Seeing is believing. They can't see their gold, can't see their money, so they've got no proof anything is real. Every practical worry above it was just that one fear wearing a different outfit.

I ran the same thing on the Festive Buyer. Different frictions, sharper ones. Digital gold doesn't feel like the real thing. It doesn't carry the same trust. There's no immediate proof. Sharing this much information feels like too much.

These rooted somewhere different. Money can come and go, but gold has always held its value. For this group, gold is the thing that survived every bank, every app, every bit of paperwork that ever failed them. So digital gold doesn't just need to be safe. It needs to be pullable on demand, the same way a locker at home is. Anything less isn't really gold to them, it's just a number on a screen.

Here's what struck me looking at both. Not one root cause was about the product's features. Every single one was about trust. Two different flavours of it, but trust all the way down.

And that difference in flavour matters, because it's what splits the two personas. Not the blocker, they share that. What's at risk behind it.

For the First Time Buyer, the risk is personal. Getting a first money decision wrong, with no experience to know if they've messed up until it's too late. For the Festive Buyer, the risk is inherited. Failing a duty handed down through generations, breaking a chain of gold that outlasted every bank and app before it.

Same blocker. Same missing proof. But one is protecting themselves, and the other is protecting something much bigger. That's the reason I built two flows, not one flow with two headlines.

Insight to plan

Turning the insight into a plan

Five Whys told me what was true about each user. It didn't tell me what to build. That's a different job, and it took two frameworks to get there.

First, Jobs To Be Done. It takes the blocker and splits it into three layers, so I'm not just solving the task but the feeling under it and the way it plays out with other people.

The row that actually earned its place was surface blocker versus real blocker.

The First Time Buyer's surface blocker is "I don't know enough." But the real one is fear of starting something new. So the job was to show how easy it is to start, and how it builds toward something.

The Festive Buyer's surface blocker is "this isn't the real gold I know." The real one is trust. So the job was to show purity, storage, certification, and the fact that it turns back into real money any time.

Those two directions, ease and future for one, purity and proof for the other, became the backbone of every screen.

Then AIPSO. This one isn't a general design tool, it's built for onboarding specifically, which is why it only shows up here.

Audience. Already settled through JTBD.

Insight. The one line blocker, from Five Whys.

Point of intervention. The exact moment I step in. Right after payment, for both.

Personalization. What changes per persona at that moment. Copy, tone, the proof I show.

System design. Three levels, manual, manual plus AI, fully AI. Onboarding stops at manual, on purpose. AI comes in later, in the second case study, where it actually pulls its weight.

I stopped onboarding at the manual level deliberately. I wanted the product thinking to stand on its own first, before any AI entered the picture. If the flows only work because something clever is generating the copy, they don't really work. So everything here is hand built. The AI comes next, and it earns a whole case study of its own.

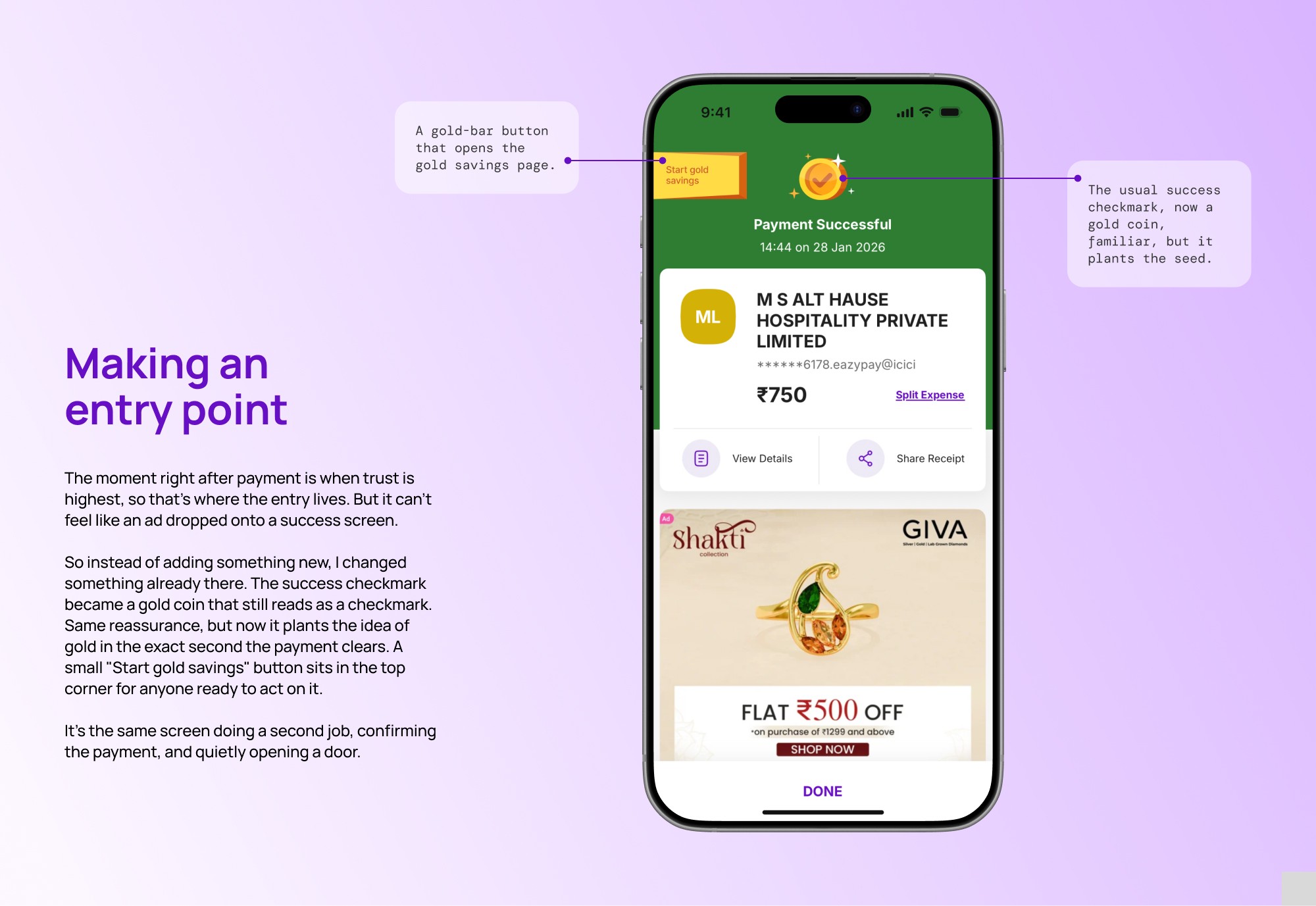

The entry point

Why right after payment

The point of intervention came from the workshop, not from me. Rajat had already established it: you step in right after payment, when the user is in a high trust state. They've just watched the app do exactly what it promised, and that afterglow is the best moment you'll get. Choosing that moment was outside my scope, so I took it as a given and designed for it.

What I did work through was why it holds up. A home banner gets scrolled past. Post KYC catches people mid admin, drained and wary. Post payment borrows trust that already exists instead of building it from scratch.

But the research didn't fully agree with itself, and that's worth being honest about. Karan said a nudge right after spending would land on him. Ramesh said he'd ignore any banner the second a payment cleared. Both are right about themselves. It doesn't sink the decision, post payment is still the strongest moment across both personas, just not a sure thing for either. So I designed for what works best on average, and let the AI layer catch the people it miss

The entry point

Post payment doesn't drop you straight into a full screen. A small nudge card shows up first, carrying the exact same headline that opens the flow. So you see what you're getting into before you tap in. No separate teaser, no bait and switch. The nudge and the first screen make the same promise, which is what keeps the entry honest.

The nudge card itself sits just outside my scope here, since the intervention point and the surface it lives on were set in the workshop. I'm noting it mainly for continuity, so the flow reads end to end.

The messaging

Hero messaging

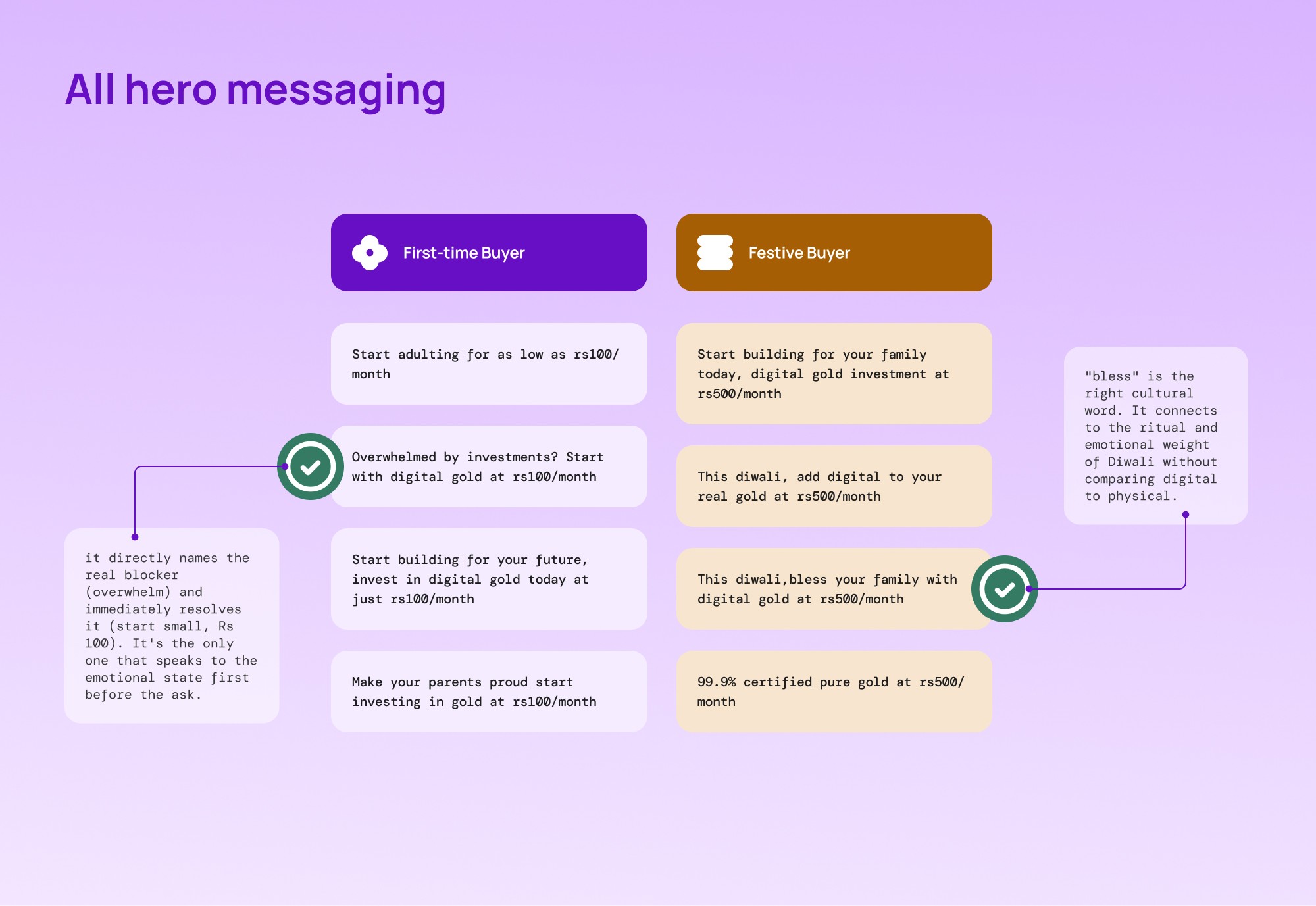

I wrote four headlines per persona and picked one from each.

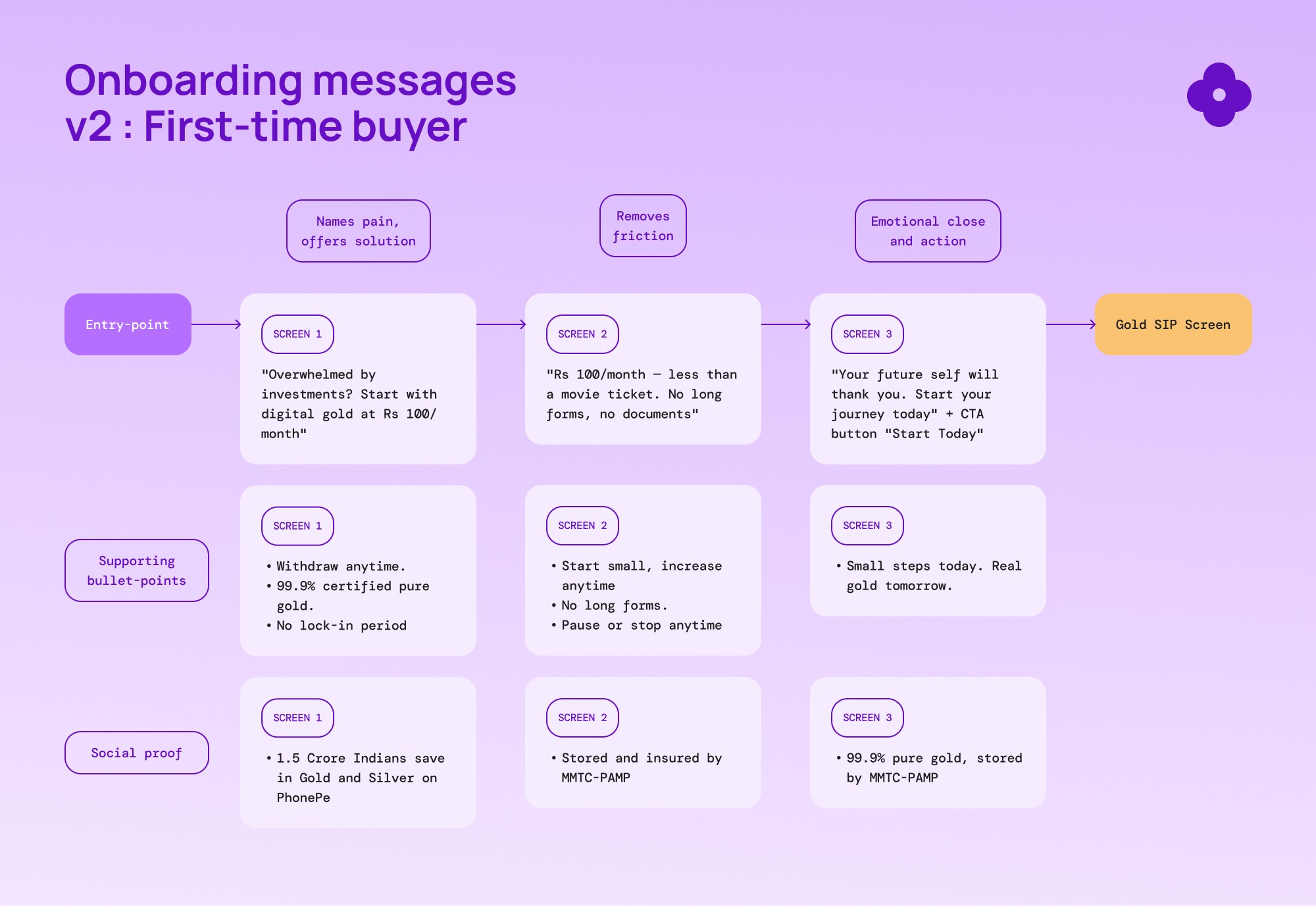

First Time Buyer, chosen: "Overwhelmed by investments? Start with digital gold at Rs 100/month."

It won because it names the fear before it makes the ask. The others either skipped the fear or piled on pressure. One of them was "make your parents proud," which turns a safe, private moment into a performance. Exactly the wrong feeling for someone who's already nervous. So it was out.

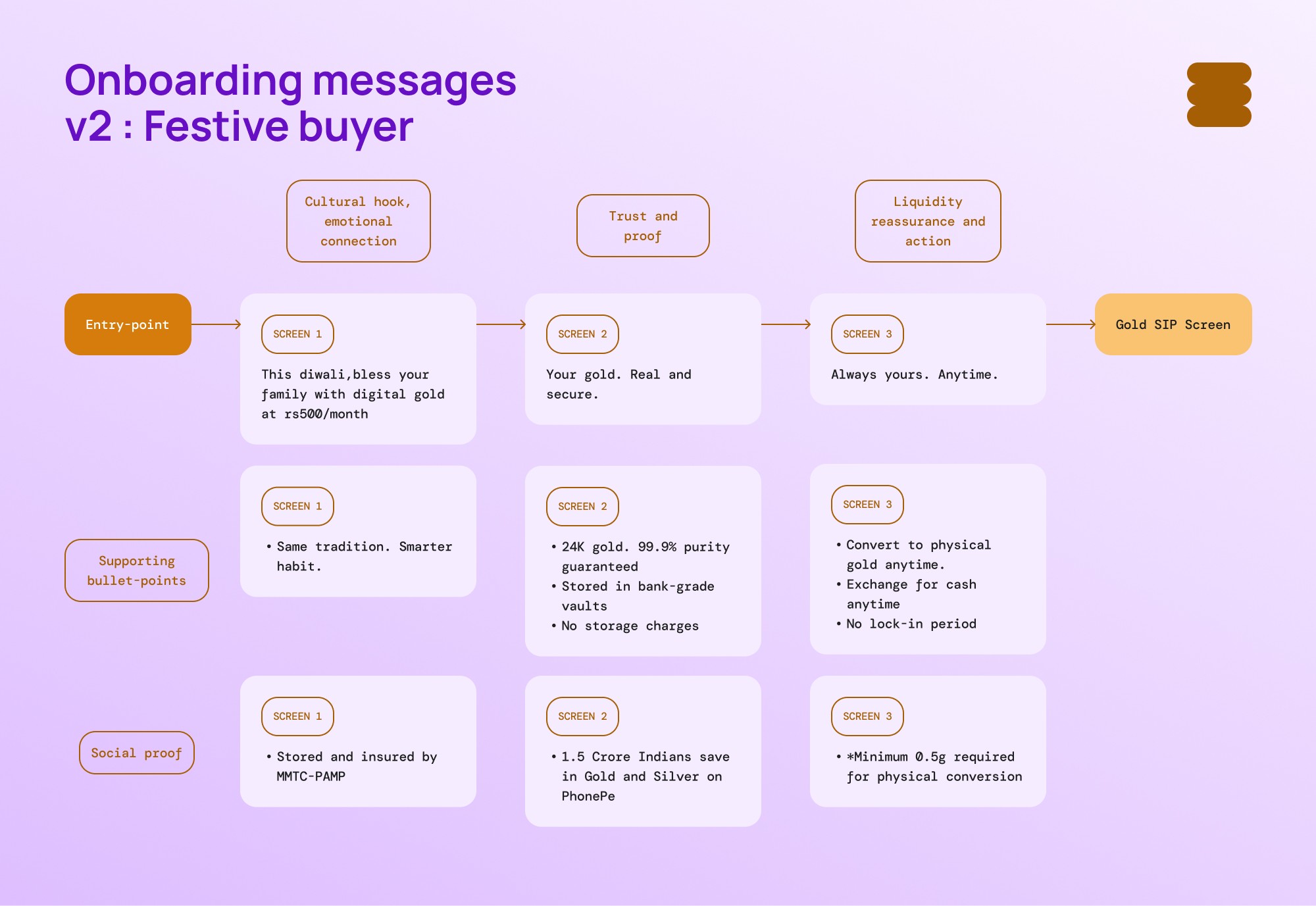

Festive Buyer, chosen: "This Diwali, bless your family with digital gold at Rs 500/month."

"Bless" carries the ritual weight of Diwali without ever comparing digital gold to physical gold. One runner up was "add digital to your real gold," which almost works, but "real" quietly implies digital isn't. That one word undercuts the whole trust argument, so I killed it.

Then the numbers. Rs 100 is just the platform floor, not a clever middle ground. The real call was whether to default the First Time Buyer there or push higher. The floor made sense, because someone early in their career already spends more than that in a day, and the fear here is overcommitting, not the amount itself. Rs 500 for the Festive Buyer was an actual choice. It works because they're already deep in festive spending, gold, clothes, all of it, so it reads as reasonable inside a season they're already in. Both adjustable once you're in the flow.

Making each screen work harder

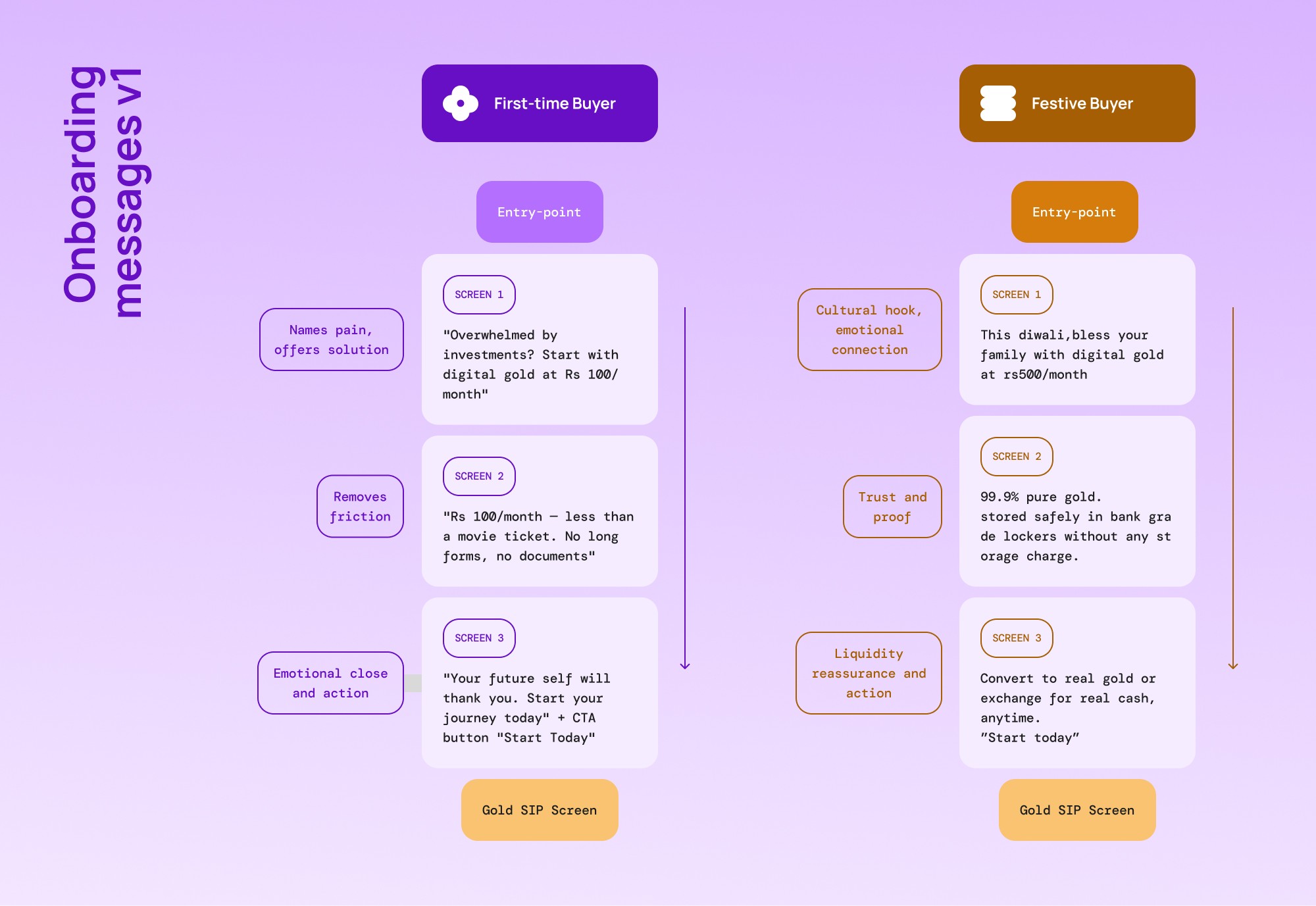

Version one was one line per screen, each doing a single job. Name the pain, offer the fix, close on emotion. It was clean. Too clean, honestly.

Because when I held it against the shared root, the problem was obvious. Both personas are being asked to hand real money to something they can't see or touch. And one line of reassurance isn't proof. It's a promise. A promise was the exact thing neither persona was willing to take at face value.

So version two didn't change what each screen was trying to do. It changed how hard each one had to work to prove it. More trust signals, placed where each persona needed them. Withdraw anytime. 99.9% certified pure gold. No lock in. Stored and insured by MMTC PAMP. The 1.5 crore users stat.

One choice worth pulling out. The Festive Buyer's second screen carries more proof than any other screen in either flow, and that's deliberate. This is the persona protecting a family's history, not just their own money, so the screen that has to win their trust had to pull more weight than anywhere else. That's the shared root showing up as an actual design decision, not just an insight sitting in a doc.

Lo-fi and routing

Lo-fi and the CTAs

Same stepper, same three screen skeleton, same layout for both personas. What changes is tone, and most of that lives in the CTAs.

The First Time Buyer climbs slowly. "Show me how," then "Let's do this," then "Start Today." Each tap asks for a little more than the last, which suits someone who needs to feel their way in rather than commit up front.

The Festive Buyer covers the same ground in fewer words. "Tell me more," then "This feels right," then "Start Today." Their trust isn't built through small steps, it's built through proof, and the proof already did its job by screen two. So the CTAs can move faster without losing them.

Illustrations stayed as gray placeholders here, on purpose. This version exists to prove the structure and the copy hold up on their own, before any visual polish gets a chance to cover for a weak flow.

The routing call I'm glad I caught

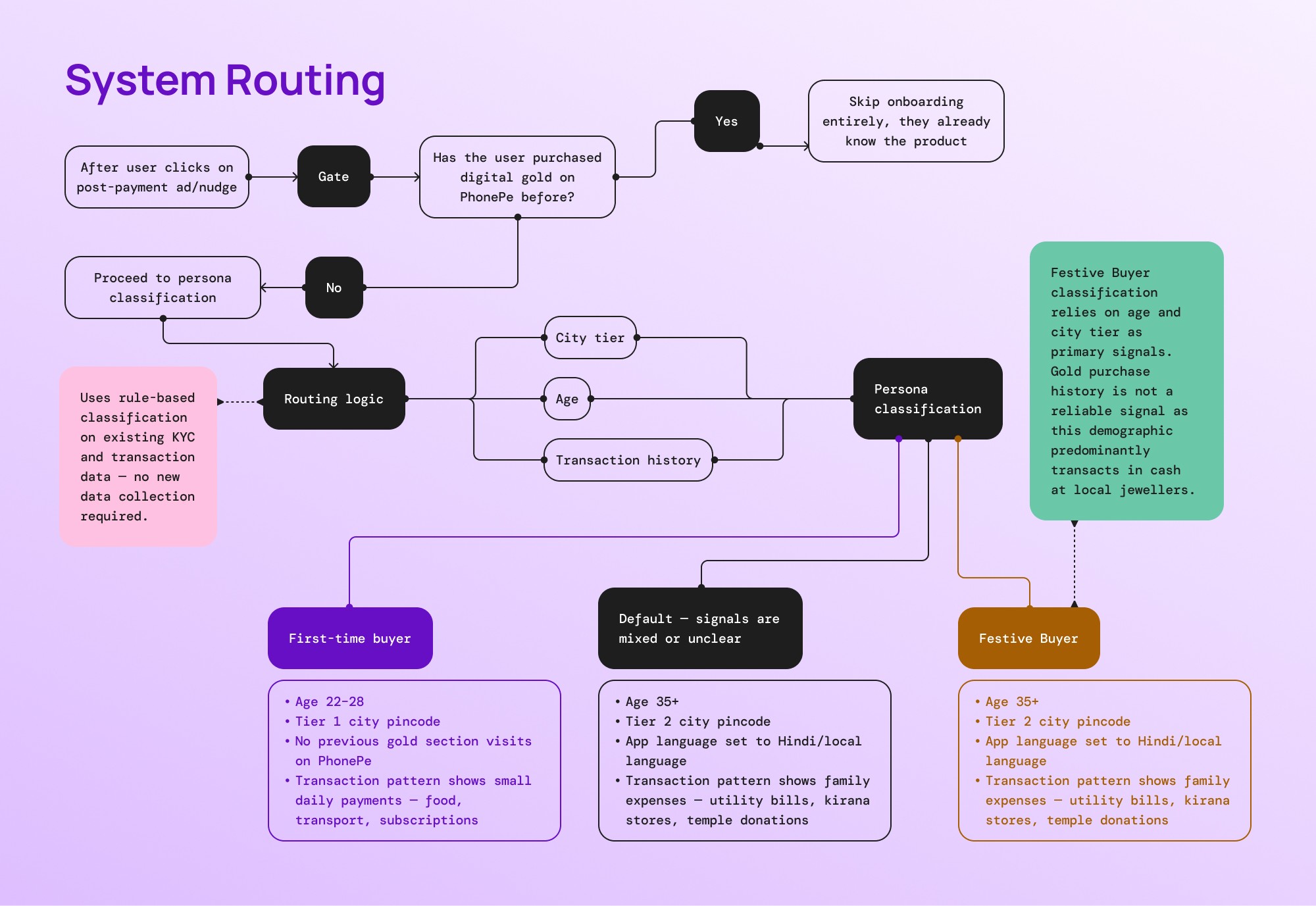

The obvious way to spot a Festive Buyer would be their gold purchase history on PhonePe. It's also completely wrong.

This group buys gold in cash, from a jeweller they've known for years. Not through an app. So their transaction history would show zero gold purchases, even though they're exactly who this flow exists for. Lean on that signal and you'd quietly filter out the very people the persona was built around. The data would look clean and the targeting would be broken.

So routing runs on signals that don't need the user to have done the one thing they'd never do on the app. A gate goes first. Have they already bought digital gold here? If yes, skip onboarding, they know the product. If no, classification runs on what's already sitting in KYC and transaction records. No new permissions, no new forms.

First Time Buyer: age 22 to 28, tier 1 pincode, no prior gold section visits, small daily spends like food, transport, subscriptions.

Festive Buyer: age 35 and up, tier 2 pincode, app language set to Hindi or a local language, spending skewed toward family, utilities, kirana stores, temple donations.

Anything that matches neither pattern drops to a generic flow, which is out of scope here.

The reviews

PM review

Like the research, this review was simulated. I ran it as a structured exercise, playing out how a senior PM at PhonePe would pressure test both flows, someone with fintech and SEBI compliance experience, focused on conversion and risk. The value isn't in it being real. It's in forcing the design to survive the kind of scrutiny it'd actually face.

The review ran against four labels: must fix, should fix, nice to have, approved. Sixteen items came back. Three are worth telling in full, because they're the ones where something actually had to be decided.

The compliance catch. "Overwhelmed by investments" got flagged must fix. Digital gold isn't a SEBI regulated investment product, and that word creates real legal exposure if a user ever disputes a loss. I reframed it to "Not sure where to start? Begin with digital gold at Rs 100/month." Same emotional beat, no regulatory risk.

The one I pushed back on. "No lock in period" got flagged as unverified, on the worry it might break if a minimum balance applied at Rs 100 entry. Instead of softening the copy to play it safe, I checked the claim against the actual product. No lock in, no minimum balance for redemption, confirmed, not assumed. The copy stayed. Conceding when you're wrong matters. So does holding your ground when you're actually right.

The Rs 500 fix. Flagged must fix, because Rs 500 stated flat with no lower entry framing reads like a fixed commitment. I added one line before screen three: you can start lower or increase anytime. Small change, removes the "locked in" feeling without weakening the number.

Everything else sorted cleanly into fixed, deferred to engineering, and approved. Nothing there needed a story, they were straightforward calls.

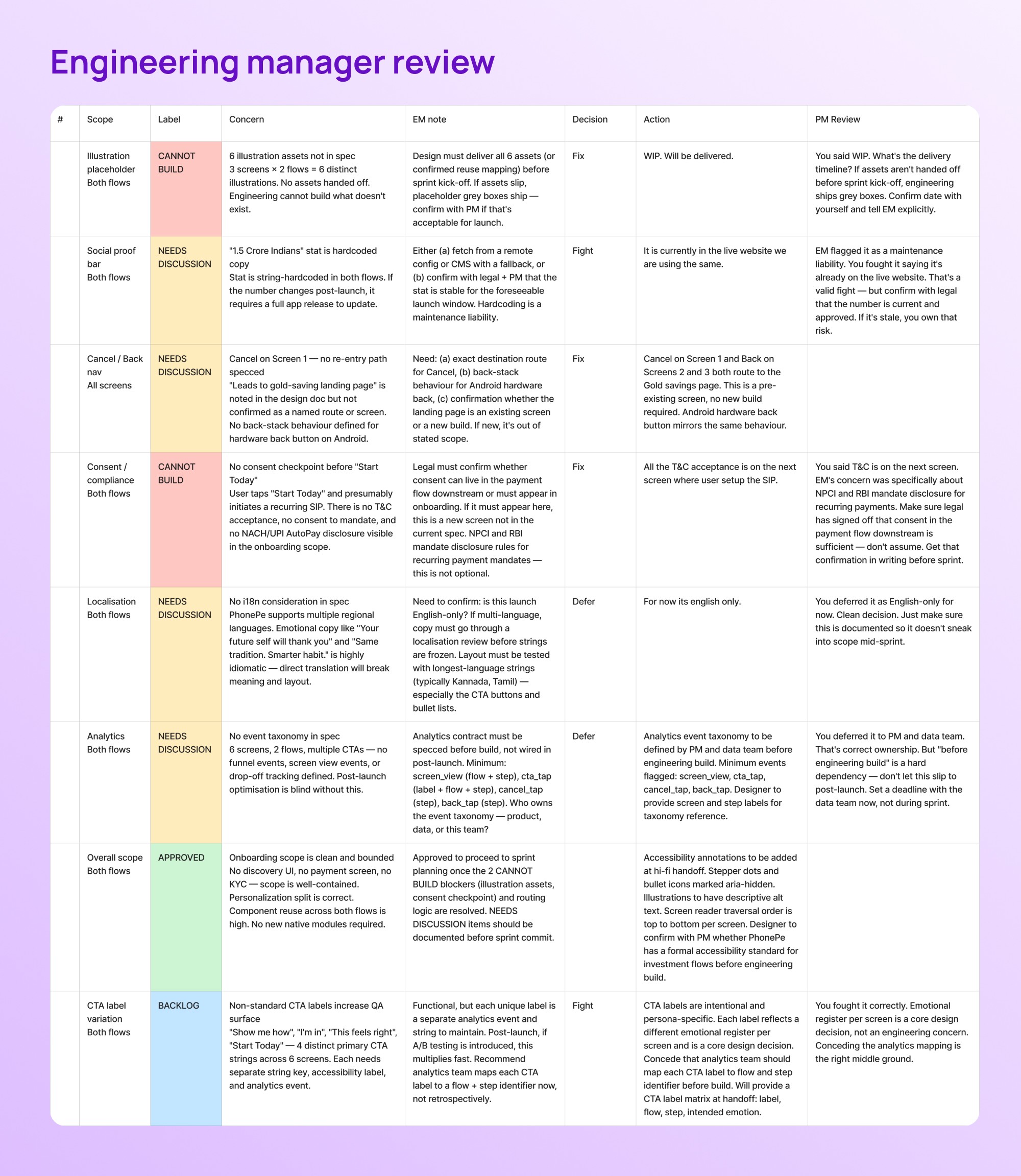

EM review

This one was simulated too, run the same way, as a senior engineering manager at PhonePe with years on payments and investment features. Then I did a second pass as the PM on top of the engineering resolutions, to check whether each fix actually held up under a second set of eyes. That back and forth is where the interesting tension showed up.

The review ran against four labels: cannot build, needs discussion, backlog, approved. Sixteen items came back. Three are worth walking through.

The stat that stayed, with a string attached. The "1.5 crore users" line got flagged as hardcoded, a maintenance risk if the number ever changes. My push back: it's already live on PhonePe's own site today, same figure. The PM's second pass accepted it but didn't let it slide free, confirm with legal that it's current, and if it goes stale, that risk sits with whoever fought to keep it. Fair condition.

The CTAs held up. The four different CTA strings got flagged as unnecessary QA surface. My push back: each label is a different emotional register per screen, that's the design, not overhead. The trade I accepted: analytics still needs every label mapped to a flow and step ID before build, delivered as a matrix at handoff, not retrofitted later. Both reviewers agreed. Creative decision held, operational cost owned.

The one that's still open. There's no T&C acceptance or mandate disclosure anywhere in onboarding, flagged cannot build. I resolved it by pointing downstream, consent lives on the SIP setup screen, not here. The PM's second pass wouldn't call that settled, because NPCI and RBI have specific rules for recurring payment mandates. The instruction was blunt: don't assume the next screen covers it, get it confirmed in writing before sprint. I'm leaving this one open, because it genuinely is.

Everything else sorted into fixed, deferred with ownership named, and approved.

From gray to gold

Making it feel like PhonePe

Lo-fi shipped with gray boxes where the illustrations go. Hi-fi's job was to fill those in and lock everything the PM and EM had settled, while staying consistent with the app users already know.

Typography and iconography came first. I matched type sizes and weights to PhonePe's existing scale rather than inventing my own, and pulled icons into the same style the app already uses, so nothing in the flow feels bolted on. The goal was for a user to not notice the seam between onboarding and the rest of the app.

For the illustrations, I built them as a system, not six one-offs. To lock the visual language, I fed a lot of screenshots of the actual PhonePe app into Gemini and ChatGPT, so the output matched their real style instead of a generic one: flat vector, slightly volumetric objects, warm backgrounds, one hero object per frame. Every gold coin carries the PhonePe पे symbol. Gold stays the brightest thing in the frame.

Then six prompts on top of that base, split by persona. The First Time Buyer got the everyday world, a desk with a bill and a coin, a movie ticket beside a coin, a piggy bank cracked open. The Festive Buyer got the cultural one, a home mandir with a diya, a red cloth pouch, an open palm holding a coin.

The correction pass. My first attempt ran on Gemini and didn't hold up, so I moved to ChatGPT for the final set. Screen one's desk came back too cluttered and too realistic, so I cut objects, flattened the shading, simplified the coin edge, then re-ran that same fix across the festive frames instead of assuming they were clean.

Scroll to the gallery below for the finished screens, or walk through the working prototypes:

→ First-Time Buyer prototype

→ Festive Buyer prototype

What's next

The onboarding is built, and built by hand. Every screen, every line of copy, every routing rule is traditional product thinking. AI helped me move faster along the way, but none of it is in the product itself. The flows would stand exactly as they are without a single AI feature underneath them. That was the point, prove the thinking holds on its own first.

Staying manual was a deliberate stop, not a limit. Rajat framed onboarding as a ladder in the workshop, from fully manual, to manual assisted by AI, to fully AI per user. This is Level 1 on purpose. The same flows could go much further, and that higher ceiling is the next case study.

Because words have a limit. A user can read every proof point and still hesitate at the moment they're meant to commit, because they still can't see it. That gap is where PAI comes in, a layer that catches them right as they're about to leave and shows them what their savings could actually grow into.

That's the end of the beginning. Onboarding tells. The next part shows.

year

2026

timeframe

21-days

tools

Figma, Claude, Gemini, ChatGPT

category

AI Assisted/Concept

01

02